The Human Condition

Week ending 4/19

I hope that everyone actually did get to spend some quality time with their family – whatever that means to each of you (you get to define quality, time, and family on your own as I’m just here for the vapid well wishing). As an aside, just to make sure that I was using the word vapid properly (I am), I came across Dan Vapid. This is almost perfect because this guy is almost exactly my age, is a punk rocker, is still going, and his current band name is “Dan Vapid and the Cheats” (after a long list of what you would think an AI generator would spit out for punk rock band names).

I am very happy to be part of Dean Curnutt’s charity event to benefit children’s education, especially in light of the heavy impact that Covid-19 has had on kids. The event is MacroMinds on May 18-19. I will be moderating a two person panel on Crypto Derivatives and get to pick the brains of Rich Rosenblum of GSR and Robert Bogucki of Galaxy. Speaking of Galaxy, Mike Novogratz will be giving the day one Keynote. There are quite a few people on the agenda whose work I’ve been reading and admiring for years. Check it out here.

Worth noting: much has been written and said about China locking down Shanghai. Certainly it is alarming to see so many people having to live under those conditions, especially when we can get such a (seemingly) clear window into life under lockdown via twitter regarding how difficult it is to get food. It was genuinely hard for me to understand. Reading/listening to Peter Zeihan recently gave me some understanding that goes beyond have some empathy for the Chinese situation. The key is to not project our experience onto China. First, our vaccines are significantly more effective overall and particularly against Omicron. US: 90+% efficacy; Chinese: originally around 51% efficacy and post-omicron under 20% efficacy (this article seems to indicate otherwise, but, for now at least, I’m going with Zeihan figures). Second, their vaccination rate is far lower. Third, due to their zero covid policy they did not have the massive outbreaks leading to exposure/immunity. All of which means that an outbreak of Omicron-B (more deadly) in a crowded city of over 20 million could be catastrophic. This is a real danger and, as distasteful and awful as lockdown is, there does not appear to be a lot of policy alternatives. It is hard to visualize the Chinese buying 50 million doses of vaccine right now: I don’t see them buying and I don’t see the US selling. The lockdown is a big issue for supply chains, of course. But it is also making the risk of a breakdown of China, either due to unrest or a massive Covid outbreak, a potential real outcome. THIS IS NOT A PREDICTION. This is an acknowledgement of risk. Please send me your reasons/evidence on why this seems a bad take.

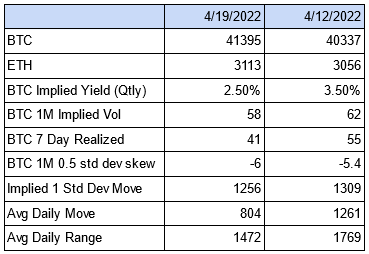

The holiday provided no fireworks at all. Certainly liquidity was low but, apparently, no one was looking to take advantage of the conditions. Most likely this is because with relatively low levels of open interest, there would not be a lot of stops/liquidations to engage. Overall right now, our market seems “cancelled due to lack of interest.”

To make a dad level turn of phrase, “lack of interest” is also the story of the basis market. Basis remains not only subdued but also very stable.

Without a catalyst, a true rise in volatility either realized or implied seems hard to imagine. Particularly with a current lack of involvement in the futures markets. This points to an uphill battle for finding multiple trading opportunities or for long vol. In the absence of that, it makes sense to take advantage of the curvature of the volatility term structure. Implied volatility from 6/24 to later months is very flat. Implied volatility from overnight to 6/24 is very steep. Buying short dates, selling Jun 24 options, and hedging some of that vega risk in Sep options has the potential do deliver value if constructed correctly.

I recommend taking a look at Dr Pippa Malmgren’s writing here on the Arctic. And I am looking forward to reading Samneet Chepal’s piece on Defi Option Vault Strategies.

Best

Ari