Guess What Day It Is ...

Week Ending July 26

Hi All,

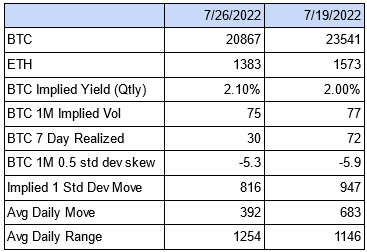

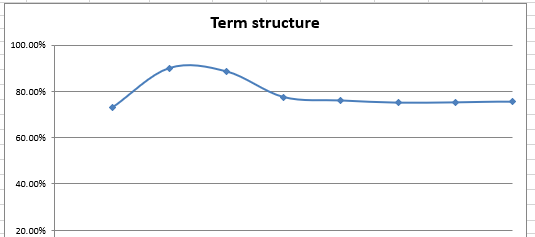

The Geico commercial with the camel and hump day and Wednesday is one of my favorites. And, it turns out, there is plenty of “hump day” going around. First, the FOMC is meeting and adjourns on Wednesday. Second, the implied volatility term structure has a “hump” in it as higher than usual expected volatility.

You can see how July 27 vol (73) and July 28 (90), and July 29 (89) form a hump and then the rest of the curve is 75-76ish. Think that the FOMC is going to be a dud? Or fireworks? What are you collecting or paying for? The good news is we can calculate the market’s implied forward volatility for the Fed meeting. The 2 second math primer: we can’t use volatility because it is the square root of variance, but the variance (which is just the vol squared) is additive, so …

7/28 forward vol = sqrt((2/365 * 0.90^2 - 1/365 * 73^2) / (1/365)) = 104%

This means that all things staying the same, when 7/27 rolls off in a few hours, that 7/28 vol would be 104%. A one day straddle at 104% is $907. A 73% one day straddle which would be $637. Interestingly, the 7/29 forward volatility is going to be very close to the 7/28 volatility since there is really not much difference between them. As an interesting aside, the 7/28 straddle is ~739 and the 7/29 is 1185 for a difference of $446. The reason that you don’t pay the full extra $907 is due to the fact that you don’t know the strike and the arbitrage continuous hedging strategy prices it that way. That does not mean you need to trade it that way. Also, keep in mind that the vols & prices were reasonable at one point today but are almost certainly wrong by the time you are reading them. An appropriate update of vols and the calcs are definitely warranted.

QCP does a nice commentary and in it, they mention the following leading up to this week’s FOMC announcement:

From the data and the current market perspective, 75 bps seems very baked in. So, on the surface, this could really be a dud of an announcement. But here is the thing: forward guidance. QCP also notes that given the economic data coming out and the market action — think commodities and the dollar not stocks — that the Fed could step back to “only” 50 bp hikes. I think that this is correct. Whether commodities are down because the market found a way to get more crude out of Russia or because China is in lockdown clamping demand or because rate hikes have crushed demand or because of the strong dollar does not matter. It is simply true that commodities are down and the dollar is very strong. Typically, political pressure pushes the Fed toward dovishness but there is some risk that the administration wants to keep pressure via strong dollar on China. But my instincts say a pullback on the trajectory of interest rates to 50bps is more likely. 50 bps is still aggressive tightening.

It’s regrettable

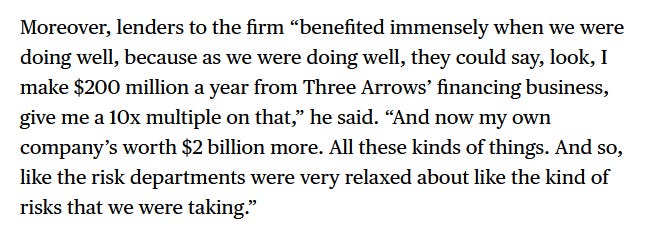

Yeah it is. I’m a fan of Byron Gilliam who writes the daily Blockworks note. Today he wrote about 3AC and that everyone was in such thrall with their genius that it was easy to be fooled by it. And I think that is partly correct. But does not go far enough. Consider what Zhu is quoted as saying in Bloomberg:

I think that this is correct. Show me the incentives and I’ll show you the outcome. Paul and I spoke about this quote over the past week. He indicated that there were rumors of fraud and that, regardless, this does not let them out of their responsibility. I have no idea if fraud was involved; certainly 3AC principals have every reason to make it seem as if there is not. I can assure you that I have no idea. But it is very easy to get people to go along with things if they have financial reasons (and 10x-ed financial reasons) to do so. It does not make Zhu and Kyle any more sympathetic characters, but this sort of thing will continue to repeat when lenders of one sort or another are aggressively incentivized to lend. Think 2008 and liar loans.

Meanwhile, oddly enough, not that much is breaking in the traditional finance world. The usual suspects, greybeards like me, warn about how the Fed raising rates after a long period of zero bound policy and QE would begin breaking things. We warn about a Minsky moment. But it seems that the worst of the excesses ended up in crypto and we rekt ourselves. Still TBD more fully.

Check it out:

Pippa Malmgren talks China, social credit, and Taiwan

I have not listened to either of these, but I’m a big fan of both Antti Ilmanen and Agustin Lebron

The Lunar Society podcast interviews Agustin Lebron on Trading, Crypto, and Adverse Selection

Tell Me I’m Wrong (please)

Ari